Tax Reform Details

Families and Individuals

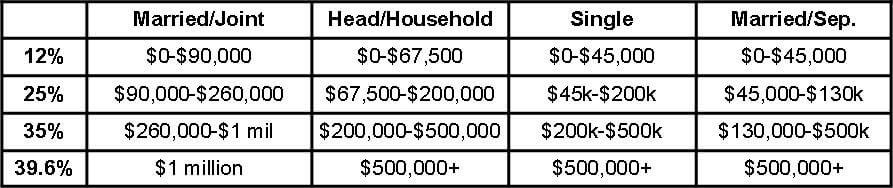

The number of tax brackets for individuals have been reduced from seven to four brackets, with the top bracket remaining at 39.6%. Preliminary break points are as follows:

The lower tax rates begin to phase-out for income in excess of $1.2 million if filing joint, $1 million of all others.

State and local income taxes will no longer be deductible. Only the first $10,000 of real estate taxes will be deductible. Mortgage interest on new mortgages will only be deductible to the extent of the first $500,000 of debt. The alternative minimum tax will go away. The estate tax will be phased-out.

Business Tax Reform

Corporate Income Tax is reduced from 35 percent today to 20 percent.

Pass-through business income would be taxed depending on the type of business and the owner’s level of activity in the business. This includes sole proprietorships, partnerships, Subchapter-S corporations, and limited liability companies.

- Personal service type business income – maximum rate of 39.6%

- Active owners in non-personal service business entities – maximum rate of 35%

- Other non-personal service business owners – maximum rate of 25%

Flow through firms earning less than $25 million can deduct interest in full. Corporations and large flow through firms are limited to an interest deduction equal to roughly 30 percent of profits.

Flow through firms can use small business expensing, which rises from $1 million to $5 million annually. All other firms can immediately expense all business investments (except buildings, land, and intangibles) for the next five years. This is known as “full business expensing.”

Ciuni & Panichi, Inc. will continue to stay abreast of the tax reform movement and will continue to keep you informed of significant changes. If you have any concerns, please contact, Jim Komos, CPA, CFP, Tax Partner, at 216-831-7171 or jkomos@cp-advisors.com